Magnera (MAGN): A Spin-Off Opportunity

Synergies, cash flow, and undervaluation make Magnera (MAGN) a compelling post-spin-off investment.

Investment Highlights (TLDR)

Significant Valuation Upside: Magnera trades at an estimated EV/EBITDA multiple of ~6x, significantly below JPMorgan’s fair value multiple of 7x and the peer average for Berry Global (BERY) and Mativ Holdings (MATV). This implies a 16%–33% upside potential, excluding synergies, growth or deleveraging.

Synergy-Driven Growth: The merger is expected to deliver $80 million in annualized synergies, valued at approximately $600 million (7.5x). These synergies could double earnings and the stock price over the next few years if realized.

Robust Free Cash Flow: I expect the combined company to generate $82 million in levered Free Cash Flow (FCF) for 2024, translating to a 13% levered FCF yield on the current market cap of $632 million. JPMorgan’s earlier analysis appears outdated, as lower interest rates and additional debt restructuring support stronger cash flow.

Deleveraging Potential: With $2.08 billion in gross debt and a weighted average cost of debt currently at 6.7%, Magnera plans to reduce net debt-to-EBITDA from 4.0-4.5x to 3.0–3.5x within three years, improving financial flexibility and driving EPS accretion.

Attractive Market Dynamics: Supported by secular trends in sustainability, hygiene, and filtration, Magnera is poised for a 3.5% revenue CAGR and 9.7% EBITDA CAGR through 2028. Key customer relationships with P&G, Kimberly-Clark, and Keurig Dr Pepper further reinforce stability and growth.

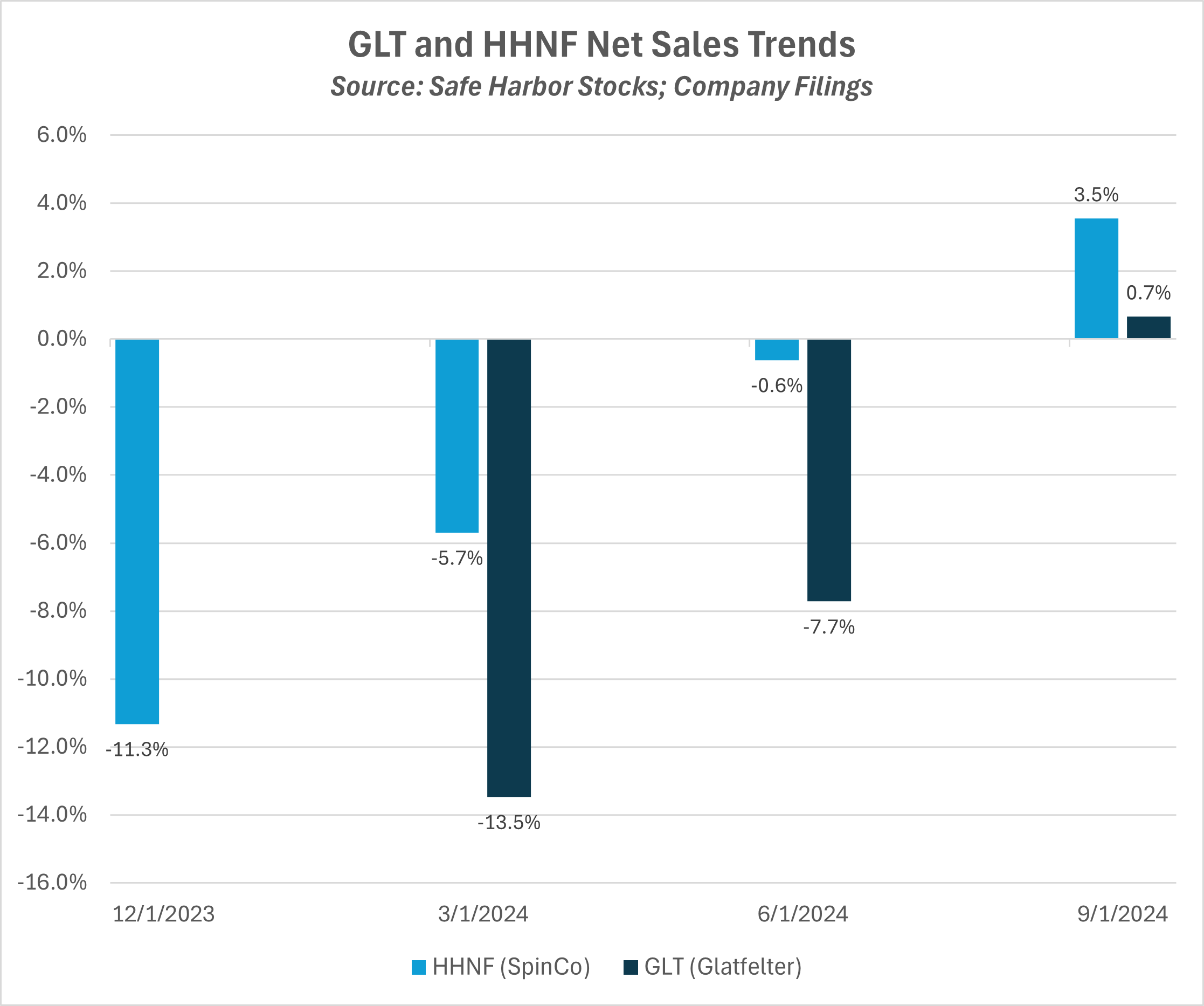

Inflection Point in Sales: After facing sales declines in 2022 and 2023 due to macroeconomic headwinds and destocking, Magnera has shown an upward inflection in recent quarters. This recovery aligns with secular tailwinds and repositioned capacity for growth.

Early Analyst Coverage: Wells Fargo very recently initiated coverage with a $22 price target, highlighting Magnera’s attractive valuation and potential. The stock currently trades (as of publication date) under $18, providing an opportunistic entry point.

Company Overview

Business Model

Magnera (NYSE: MAGN) produces nonwoven and engineered materials serving diverse end-markets, including hygiene, healthcare, and industrial applications. Key products include filtration media, hygiene materials, and specialty papers. Think disposable items such as diapers and Keurig coffee filters.

Formation Through Spin-Off and Merger

Magnera was formed in November 2024 through the spin-off of Berry Global’s Health, Hygiene, and Specialties (HHNF) segment, which subsequently merged with Glatfelter Corporation’s engineered materials business. This strategic combination created a newly listed specialty materials leader with enhanced scale, diversified markets, and a compelling synergy opportunity.

Key Segments

Hygiene and Healthcare Materials: Nonwoven fabrics for personal hygiene, medical wipes, and incontinence products.

Industrial Applications: Specialty papers and materials for construction, filtration, and packaging.

Competitive Position: Magnera is a leader in the specialty materials industry, leveraging economies of scale, established customer relationships, and a strong innovation pipeline.

Investment Thesis

Core Growth Drivers

Secular Tailwinds: Increasing demand for sustainable materials, hygiene products, and filtration solutions supports consistent revenue growth.

Customer Relationships: Major clients like P&G, Kimberly-Clark, and Keurig Dr Pepper provide stable demand and long-term contracts.

Post-Merger Synergies: $80M in annualized synergies will drive EBITDA growth and enhance margins.

Excess Capacity: Russia and Ukraine accounted for 7% of Glatfelter’s sales in 2021 before the war broke out. It’s repurposed some of this, but excess capacity remains available, minimizing new capex for near-term sales growth.

Competitive Advantages

Scale and Scope: The combined entity has a diversified customer base and operates across high-growth markets.

Resilient Free Cash Flow: SpinCo maintained a 7.5% FCF margin in 2023 despite sales declines, highlighting operational efficiency.

Innovation: Focus on sustainable, bio-based materials aligns with evolving customer preferences.

Capital Allocation

Management is prioritizing synergies, debt reduction, and reinvestment in R&D to support future growth. Deleveraging to a 3x net debt-to-EBITDA ratio within three years is expected to drive EPS accretion and valuation re-rating.

Management plans to target a 3x net debt-to-EBITDA ratio within three years, down from about 4.0-4.5x today depending on your EBITDA estimate. It also has a $350 unused revolver and no debt maturities until 2029.

Risks to Thesis

Integration challenges in realizing synergies.

Revenue concentration risk with large customers in markets that experienced COVID tailwinds, though I believe we have far lapped those base effects.

Sensitivity to raw material costs and macroeconomic headwinds. Sales declined in 2022 and 2023 but have now seen an inflection upward in recent quarters.

Net Sales Trends

The latest prospectus dated September 20, 2024, mentions modest YTD revenue declines and this is true on a 9-month basis. However, I spent some time digging into the quarterly releases for each of GLT and HHNF - and we have an interesting inflection in sales growth illustrated by the chart below on a YoY quarterly basis. Note below that I could not obtain sufficient data for the December 2023 quarter for GLT YoY.