Why Add-Back Stock-Based Compensation?

A Study of Free Cash Flow and SBC Using PayPal

Adding back stock-based compensation (SBC) when calculating free cash flow (FCF) may seem controversial. It’s one of many non-GAAP adjustments that management can manipulate. However, it is a rational approach once you understand the entire picture. Stock-based compensation has unique implications for FCF and equity dilution that deserve a closer look. Let’s break it down using PayPal as a case study.

Free Cash Flow and Its Components

Free cash flow (FCF) lacks a universally accepted definition, and interpretations often vary. I will first outline my own definition and methodology, which I believe is most sensible.

For our purposes, I refer only to levered cash flow, sometimes known as Free Cash Flow to Equity (FCFE), which accounts for debt-related costs.

Below is the general formula we’ll work with to begin, and I will add my variations as we proceed.

Stock-Based Compensation (SBC) and CFO

Within net cash from operations (CFO), SBC is typically added back to net income since it doesn’t involve a cash outflow. However, critics argue this adjustment overstates valuation metrics, especially in discounted cash flow (DCF) analyses. While I avoid conducting DCF analysis due to their reliance on subjective and blunt assumptions, SBC’s role in FCF still requires thoughtful consideration. In fact, I would argue that including the effect of SBC (i.e., not adding it back) may actually understate certain metrics.

Notice the SBC denoted in the image below from PayPal’s latest SEC filing. The $947 million figure comprises about 19% of total CFO ($5.056 billion in the image) during the nine-month period. SBC represents a material percentage of CFO, so it is important to truly understand how to treat it.

If we consider FCF per share as a metric, then FCF is our numerator. The CFO of $5.056 billion above includes the SBC add-back and we should leave this as is. SBC is a non-cash expense and represents an equity claim rather than an income statement expense. As such, its impact should be reflected differently as you will see further below using the last twelve months (LTM) of financials.

Capital Expenditures

Capex is another concept that requires some clarification. It is subtracted from CFO to give our FCF value. Many sources, including the companies themselves, subtract all capex from CFO to arrive at free cash flow. I find this particularly short-sighted. There are two kinds of capex that we should distinguish between:

Maintenance (or Sustaining) Capex: Required to sustain current operations.

Growth Capex: Investments for expansion.

Some companies do not break out these categories, making more conservative assumptions necessary. We have a couple of workaround options for this.

First, we could simply use the entire capex amount. This is the approach taken by providers such as Koyfin and companies such as PayPal. If anything, it is a bit more conservative since it potentially understates FCF by including some growth capex.

Alternatively, we can utilize depreciation and amortization expense as a proxy for maintenance capex. This theory relies on the fact that management depreciates its capex over an estimated useful life, which acts as a proxy for its maintenance and ultimate replacement to maintain current operations. However, one must be careful as there are many flavors of amortization expense, and we don’t want to include all of those.

Below you can see that the D&A for PayPal for the nine months ended 9/30/2024 is $783 million compared to capex (purchases of property and equipment) of $480 million. Sometimes you will see the D&A materially higher or lower than the capex.

If management does not break out maintenance capex explicitly then I often prefer the first approach above, but that can depend upon the industry type and company’s growth strategy.

Why Add-Back SBC?

Now let’s look at why it makes sense to add-back SBC. Remember we are focused on FCF not earnings, which is a separate yet similar discussion.

As previously mentioned, SBC is a non-cash expense so it can underestimate FCF by not adding it back. However, it’s still a form of compensation and we must hold SBC to that standard. It is an additional claim on equity (share dilution) rather than an income statement expense. So, it belongs in the denominator of a FCF metric, not the numerator.

For example, in FCF per share it affects the shares outstanding, not the FCF itself. Including the effect of SBC in both would be double counting.

PayPal’s LTM FCF Per Share: An Illustration

We’ll evaluate this idea through the lens of PayPal again. For the last 12 months PayPal brought in free cash flow of $7.05 billion as seen below in the Current/LTM column. This figure already includes the add-back of SBC into CFO. I include SBC as a separate line item on top for the context of our discussion. It represents 17% of CFO.

Note: I did verify the accuracy of all these figures with PayPal’s actual SEC filing. I encourage you to do the same in your own analysis - verify as close to the source as possible.

Based on the image above, it is a simple subtraction problem to find FCF: CFO of $7.67 billion less Capex of $625 million equaling $7.05 billion of FCF for our numerator.

Over the LTM PayPal had approximately 1.057 billion weighted-average diluted shares outstanding (our denominator) giving us FCF per share of $6.67.

The Denominator Matters

You may notice that above Koyfin reports a different FCF per share of $7.00 for LTM, and I believe this is due to the denominator it uses for diluted shares outstanding. Koyfin apparently uses the ending share count for the most recent quarter (1.006 billion shares). This isn’t the most conservative and rational approach as the result reflects all the benefit of additional share repurchases through the end of the period. It is not a weighted average.

As you can see, even slightly different methods for share count can lead to material differences in FCF per share, and consequently any related metrics. Such nuances highlight the importance of understanding both the numerator and denominator in FCF metrics.

You can check my $6.67 per share calculation by dividing, in the image below, $7.045 billion by 1.057 billion shares in the LTM column. It yields $6.67 per share because it calculates a weighted average based on each particular quarter’s share count. It weights the higher share count from earlier quarters before later buybacks were deployed.

The block quote above shows a 4.7% difference in FCF per share, and we haven’t yet addressed our most important question: how do we account for the effect of SBC in the denominator?

Accounting For SBC

We account for stock-based compensation through the denominator - the share count. Fortunately, the share count already reflects the effect of SBC during the period.

When you see SBC expensed on the income statement and added back on the cash flow statement, it means that the shares have already been added to the total share count. Thus, no adjustment is required to the denominator. See an example with PayPal below.

I highlighted the additions to share count above in yellow for the last nine months of 2024. There are three reported issuances, one for each quarter: 6 million, 3 million and 2 million shares. These shares represent the actual share dilution for PayPal equity investors before any repurchases. THIS is what we must account for! We also add an additional 1 million shares, based on the issuance from Q4 2023, giving us a total of 12 million shares issued for the LTM period.

The weighted-average diluted share count of 1,057 billion cited earlier includes this additional issuance, and so does the ending share count of 1,006 billion as of 9/30/2024. Thus, our FCF per share metric remains the same at $6.67 per share.

The SBC expensed on the income statement is simply an accounting formality prescribed by FASB to estimate the dollar value of compensation as the shares are vested or exercised. In fact, the actual value is quite different and varies as much as the share price itself. Furthermore, the value should not even be recorded in FCF or earnings.

If so inclined, one can estimate the financial cost by taking the weighted-average price of PYPL stock over the last twelve months and multiplying it by 12 million shares. For example, let’s estimate that the average stock price was $63 per share. This yields $756 million which happens to be much less than the SBC expense. This discrepancy is likely attributable to the fact that the underlying stock price was higher on the grant date than it’s been during the vesting period on average.

Regardless, this cost should not be recorded as it is a dilution of existing equity ownership only. The effects should only show in the per share metrics.

Interestingly, until 2006 companies did not expense SBC at all. The only requirement was a disclosure of SBC in the footnotes. My only guess as to why FASB required this under FAS 123R was to discourage excess shareholder dilution and manipulation by companies. I believe there are better ways to achieve this objective.

The inclusion of SBC as an expense as required by FASB does provide a benefit to companies via a tax benefit. SBC expense reduces taxable income, and this can have a noticeable effect on a company’s effective tax rate - sometimes flipping it from an expense to a tax benefit.

Additionally, there is a cash outflow component to SBC in the financing section of the cash flow statement. This arises from situations such as proceeds received from stock options being exercised or tax withholding paid on settling Restricted Stock Units (RSUs). We’ll leave this topic for another article.

This section is effectively a long way to say: add back SBC to FCF and leave the denominator as it is.

Unvested RSUs

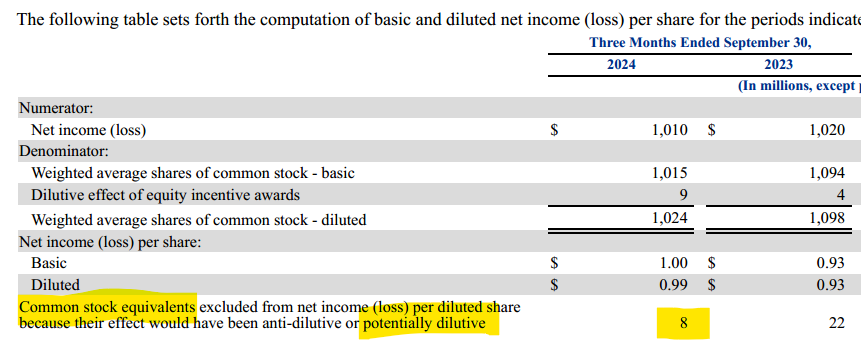

There is one more aspect we must cover and it relates to unexercised employee stock options and unvested RSUs. The stock options are trickier to understand, and PayPal predominantly uses RSUs. So I will stick to RSUs here.

In the Notes to the Financial Statements, companies will report any common share equivalents excluded from net income per diluted share. In the case of PayPal, it excludes any unvested RSUs from its diluted share count. For the three months ended 9/30/2024, PayPal reported 8 million shares excluded because the units were unvested.

If PayPal continues to perform well, we may expect these performance-based RSUs to ultimately vest. Therefore, it may be more conservative to include them in the share count. We can only estimate this exclusion of shares on a LTM basis. The last nine months shows 12 million additional shares excluded. Using this would drop FCF per share down to $6.59 from $6.67. [$7.045 billion / (1.057 + .012 billion shares) = $6.59/share]

The unvested RSUs are also an important consideration in a DCF analysis for those who conduct it. It can help project future share dilution and assess the sustainability of SBC practices.

Conclusion

Free cash flow is a cornerstone of financial analysis, yet its calculation requires careful attention to nuances like SBC and Capex. Evaluating the financial statements of a company can be complex. It involves understanding and maneuvering through various accounting regulations and management adjustments.

Adding back SBC appears rational for determining FCF and perhaps net income as well. It’s important to avoid double counting SBC and understanding how SBC affects equity investors in the denominator.

There are good reasons for a company to use SBC responsibly so long as it is not abused and contributes to FCF per share growth in the long term.

Thanks for being part of the Safe Harbor community! Follow me for more insights: LinkedIn | X (formerly Twitter)

Disclosures:

This information is provided for informational purposes only and should not be considered a solicitation or recommendation to buy or sell any securities. The author or entity providing this information may hold positions in the securities discussed. This is not investment advice.

The Koyfin link(s) above is a referral link. If you don’t yet use Koyfin but are interested, you can get 10% off by using the link. I am not affiliated with Koyfin; I simply like their app and use it every day for my own investing.